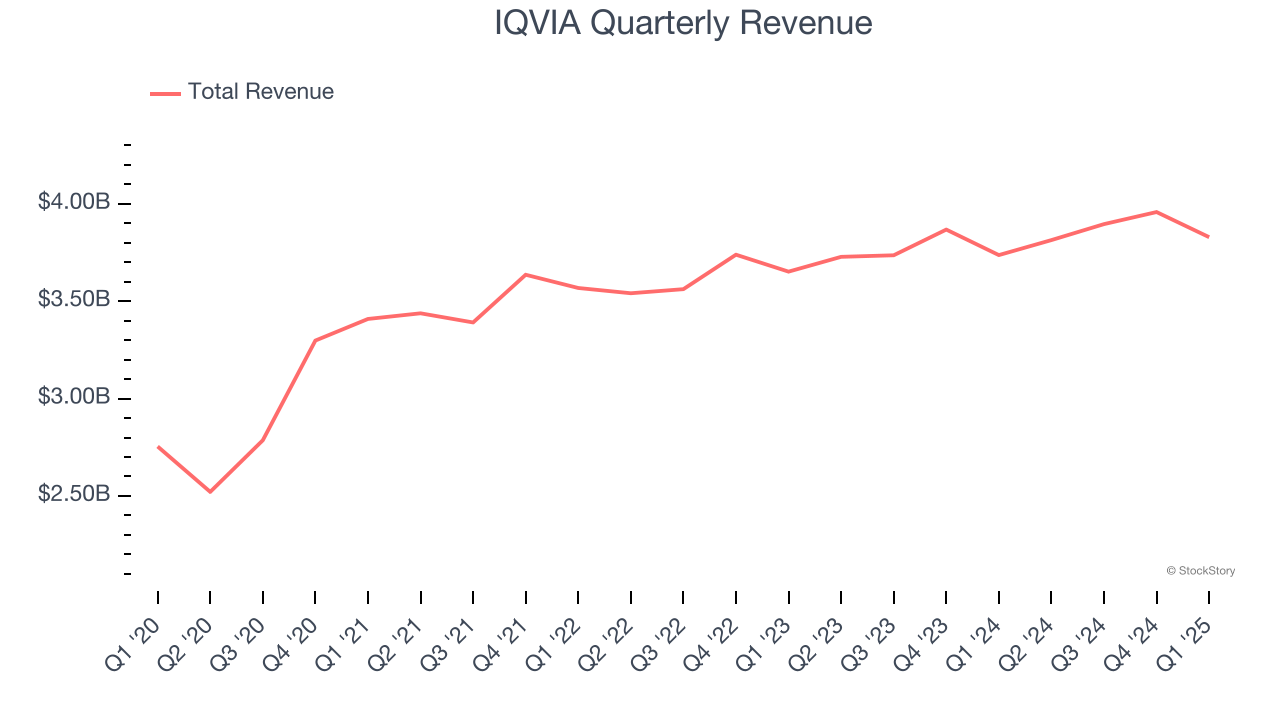

Clinical research company IQVIA (NYSE: IQV) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 2.5% year on year to $3.83 billion. The company’s full-year revenue guidance of $16.2 billion at the midpoint came in 2.1% above analysts’ estimates. Its non-GAAP profit of $2.70 per share was 2.6% above analysts’ consensus estimates.

Is now the time to buy IQVIA? Find out by accessing our full research report, it’s free.

IQVIA (IQV) Q1 CY2025 Highlights:

- Revenue: $3.83 billion vs analyst estimates of $3.77 billion (2.5% year-on-year growth, 1.5% beat)

- Adjusted EPS: $2.70 vs analyst estimates of $2.63 (2.6% beat)

- Adjusted EBITDA: $883 million vs analyst estimates of $880.3 million (23.1% margin, in line)

- The company lifted its revenue guidance for the full year to $16.2 billion at the midpoint from $15.93 billion, a 1.7% increase

- Management reiterated its full-year Adjusted EPS guidance of $11.90 at the midpoint

- EBITDA guidance for the full year is $3.83 billion at the midpoint, in line with analyst expectations

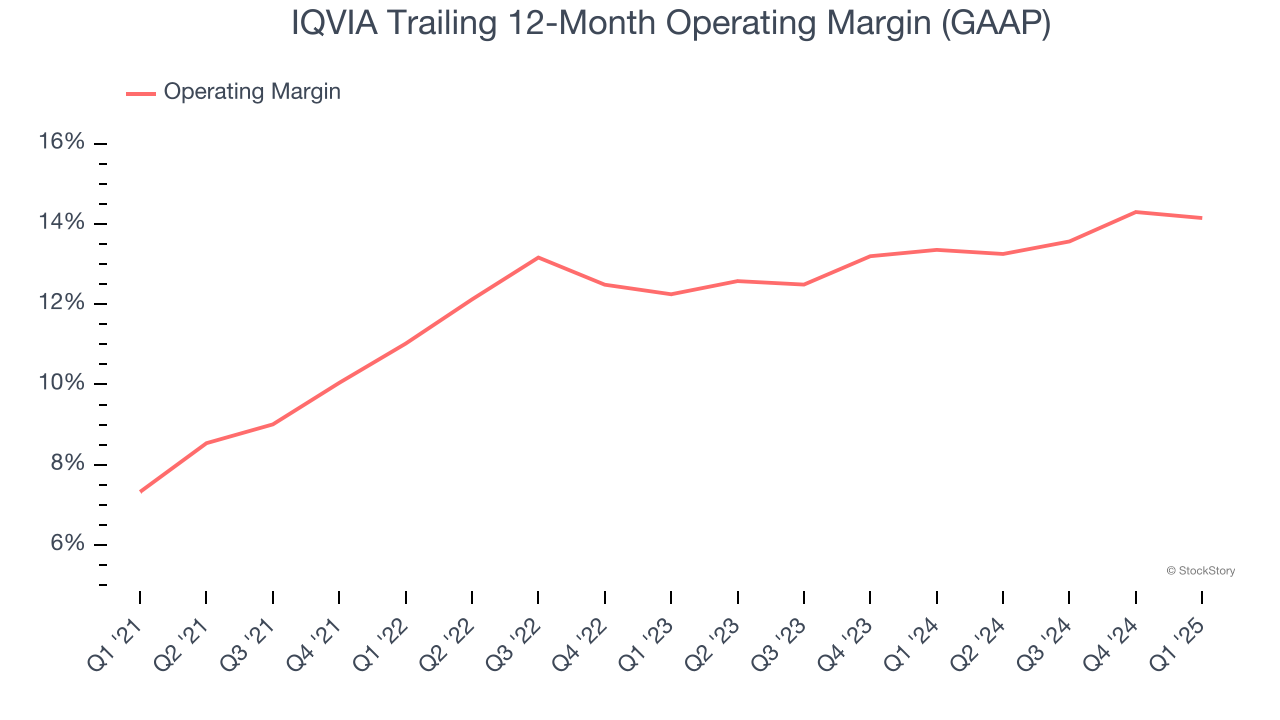

- Operating Margin: 13%, in line with the same quarter last year

- Free Cash Flow Margin: 11.1%, up from 10.1% in the same quarter last year

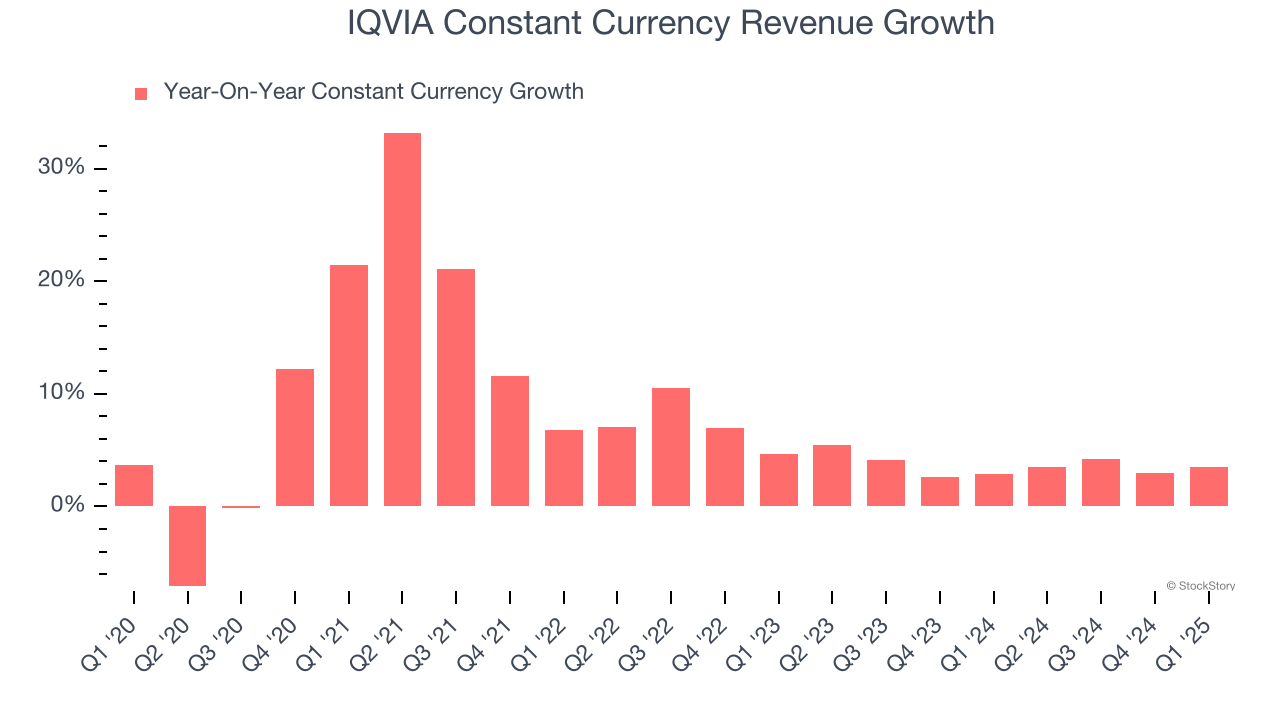

- Constant Currency Revenue rose 3.5% year on year, in line with the same quarter last year

- Market Capitalization: $26.85 billion

Company Overview

Created from the 2016 merger of Quintiles (a clinical research organization) and IMS Health (a healthcare data specialist), IQVIA (NYSE:IQV) provides clinical research services, data analytics, and technology solutions to help pharmaceutical companies develop and market medications more effectively.

Sales Growth

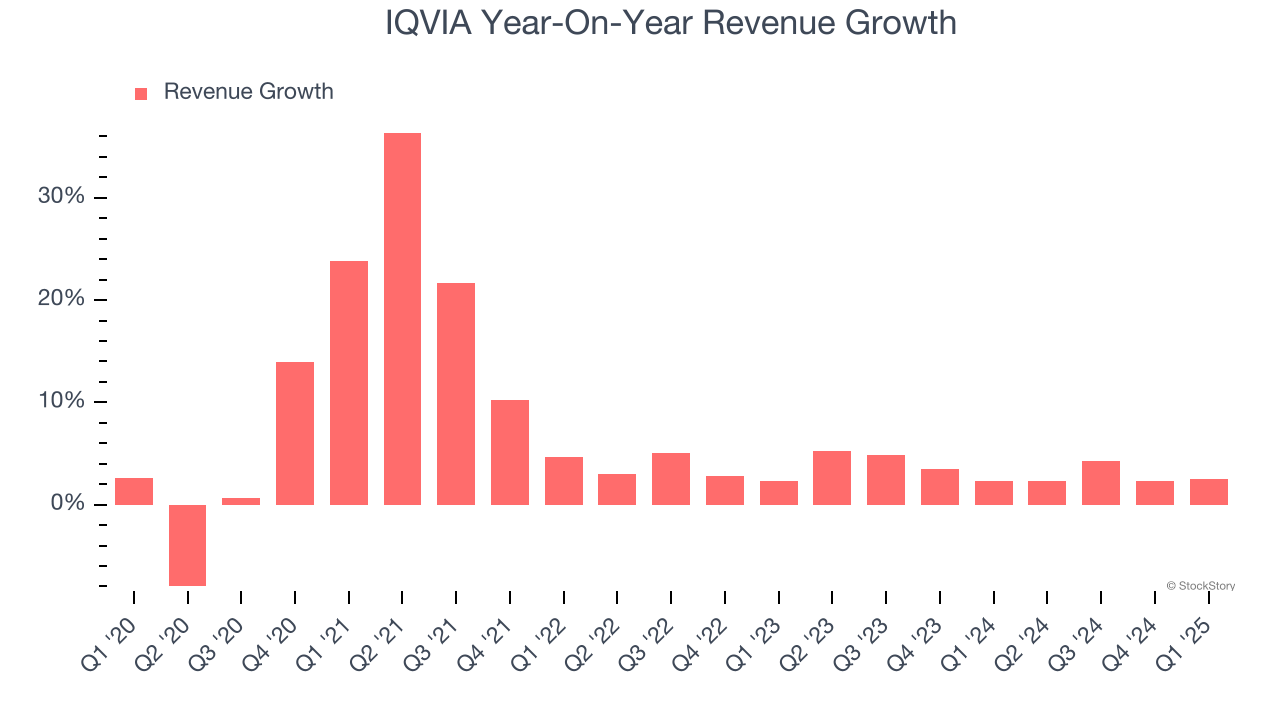

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, IQVIA grew its sales at a mediocre 6.8% compounded annual growth rate. This was below our standard for the healthcare sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. IQVIA’s recent performance shows its demand has slowed as its annualized revenue growth of 3.4% over the last two years was below its five-year trend.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.7% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that IQVIA has properly hedged its foreign currency exposure.

This quarter, IQVIA reported modest year-on-year revenue growth of 2.5% but beat Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not catalyze better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

IQVIA has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 11.8%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, IQVIA’s operating margin rose by 6.8 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 1.9 percentage points on a two-year basis.

In Q1, IQVIA generated an operating profit margin of 13%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

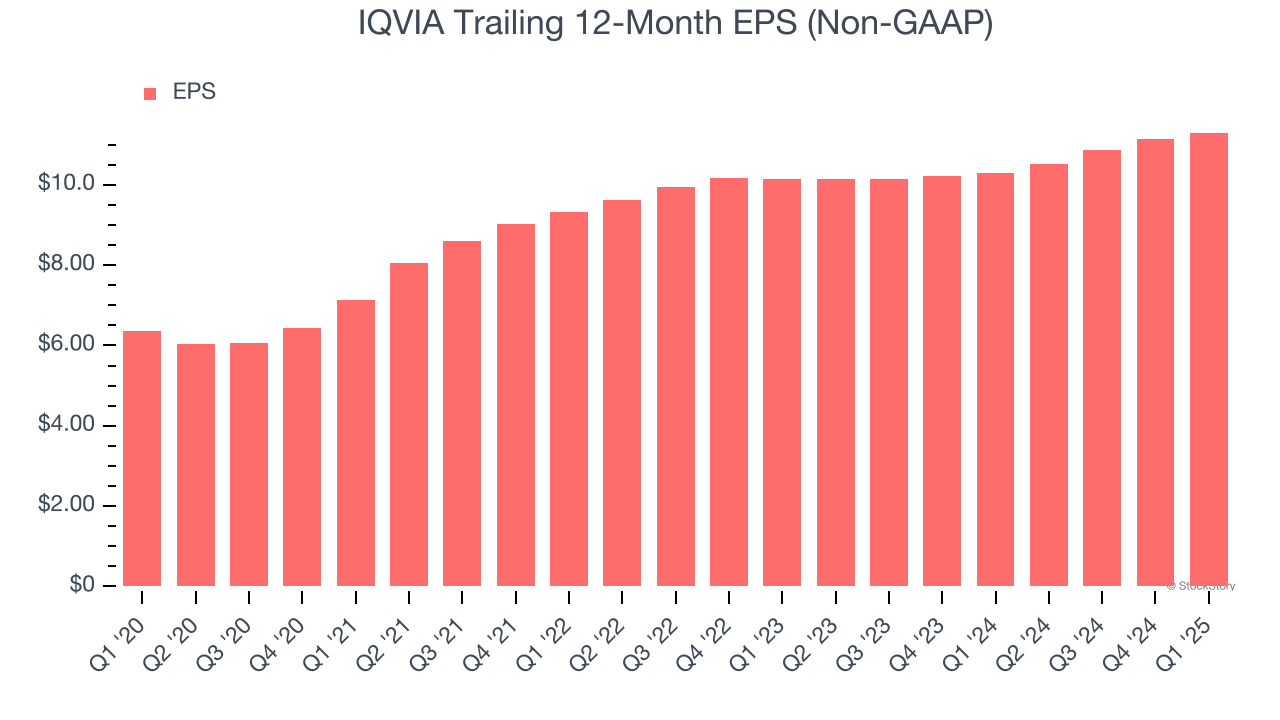

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

IQVIA’s EPS grew at a spectacular 12.1% compounded annual growth rate over the last five years, higher than its 6.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

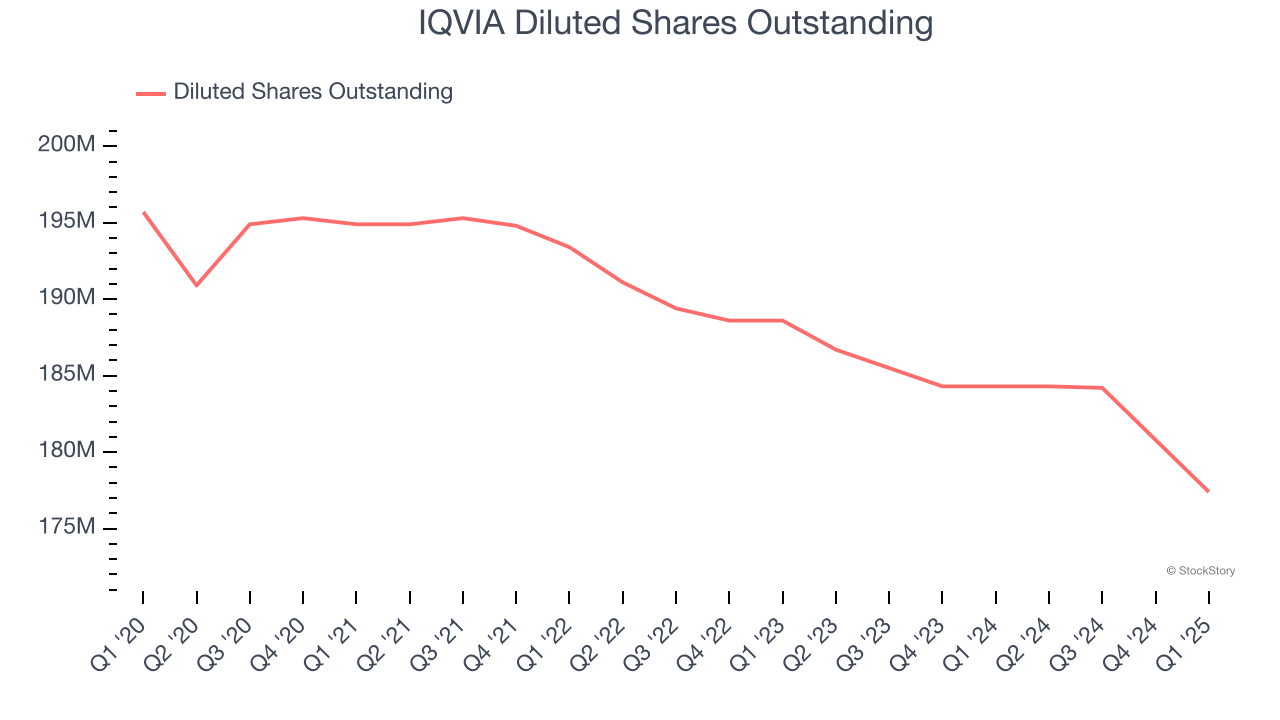

Diving into IQVIA’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, IQVIA’s operating margin was flat this quarter but expanded by 6.8 percentage points over the last five years. On top of that, its share count shrank by 9.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, IQVIA reported EPS at $2.70, up from $2.54 in the same quarter last year. This print beat analysts’ estimates by 2.6%. Over the next 12 months, Wall Street expects IQVIA’s full-year EPS of $11.30 to grow 7.8%.

Key Takeaways from IQVIA’s Q1 Results

It was great to see IQVIA’s full-year revenue guidance top analysts’ expectations. We were also happy its constant currency revenue narrowly outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 3% to $157 immediately following the results.

IQVIA may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.