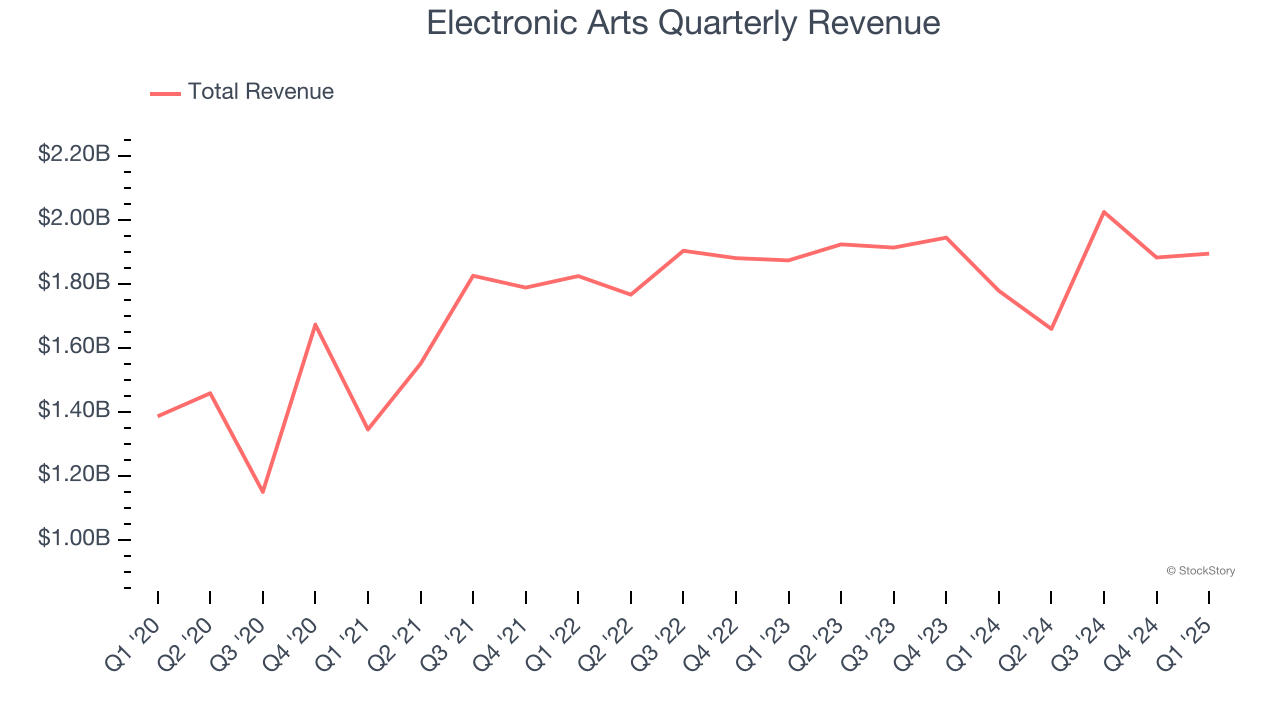

Video game publisher Electronic Arts (NASDAQ:EA) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, with sales up 6.5% year on year to $1.90 billion. The company expects next quarter’s revenue to be around $1.6 billion, coming in 10.6% above analysts’ estimates. Its GAAP profit of $0.98 per share was 8.2% above analysts’ consensus estimates.

Is now the time to buy Electronic Arts? Find out by accessing our full research report, it’s free.

Electronic Arts (EA) Q1 CY2025 Highlights:

- Revenue: $1.90 billion vs analyst estimates of $1.76 billion (6.5% year-on-year growth, 7.6% beat)

- EPS (GAAP): $0.98 vs analyst estimates of $0.91 (8.2% beat)

- Management’s revenue guidance for the upcoming financial year 2026 is $7.3 billion at the midpoint, missing analyst estimates by 3.9% and implying -2.2% growth (vs -1.1% in FY2025)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $3.44 at the midpoint, missing analyst estimates by 23.4%

- Operating Margin: 20.8%, up from 13.2% in the same quarter last year

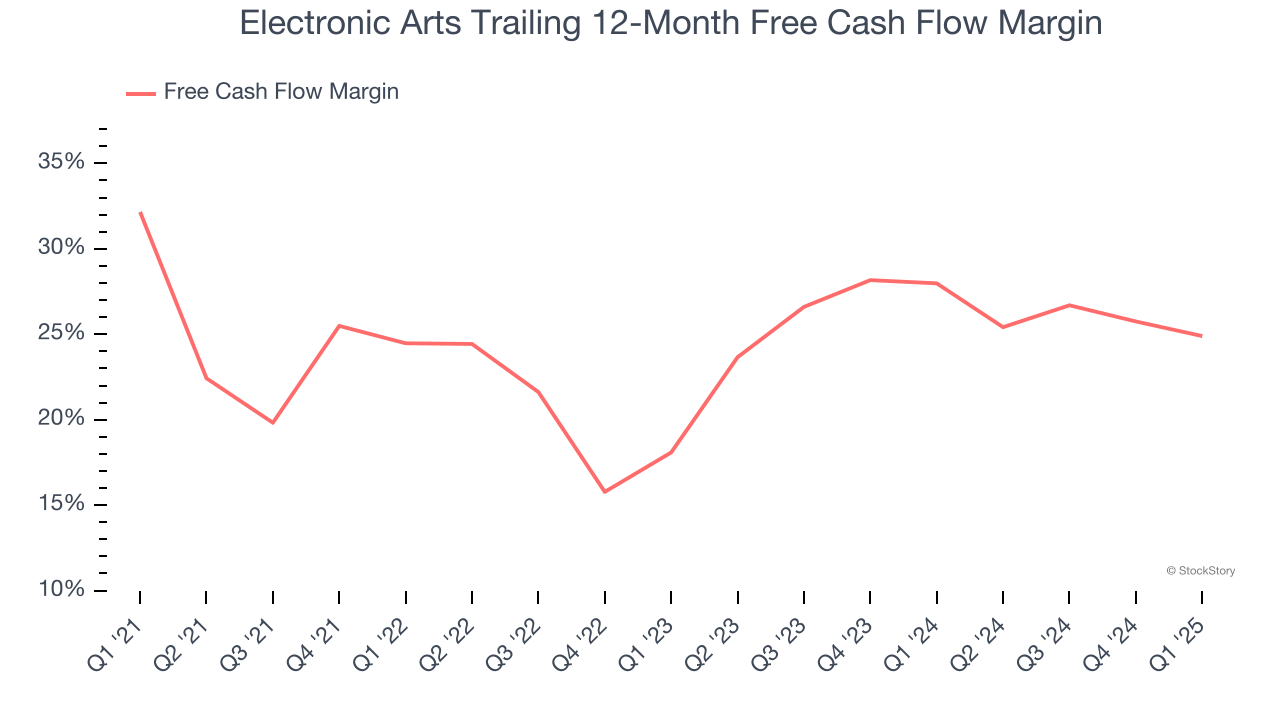

- Free Cash Flow Margin: 26.1%, down from 59.8% in the previous quarter

- Market Capitalization: $40.33 billion

Company Overview

Best known for its Madden NFL and FIFA sports franchises, Electronic Arts (NASDAQ:EA) is one of the world’s largest video game publishers.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Electronic Arts grew its sales at a sluggish 2.2% compounded annual growth rate. This wasn’t a great result, but there are still things to like about Electronic Arts.

This quarter, Electronic Arts reported year-on-year revenue growth of 6.5%, and its $1.90 billion of revenue exceeded Wall Street’s estimates by 7.6%. Company management is currently guiding for a 3.6% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.7% over the next 12 months, similar to its three-year rate. This projection is underwhelming and implies its newer products and services will not catalyze better top-line performance yet. At least the company is tracking well in other measures of financial health.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Electronic Arts has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 26.4% over the last two years.

Taking a step back, we can see that Electronic Arts’s margin was unchanged over the last few years, showing its long-term free cash flow profile is stable.

Electronic Arts’s free cash flow clocked in at $495 million in Q1, equivalent to a 26.1% margin. The company’s cash profitability regressed as it was 3.6 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Key Takeaways from Electronic Arts’s Q1 Results

It was great to see Electronic Arts’s revenue and EPS beat analysts’ expectations. On the other hand, its full-year revenue and EPS guidance fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 6.1% to $164 immediately after reporting.

Indeed, Electronic Arts had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.