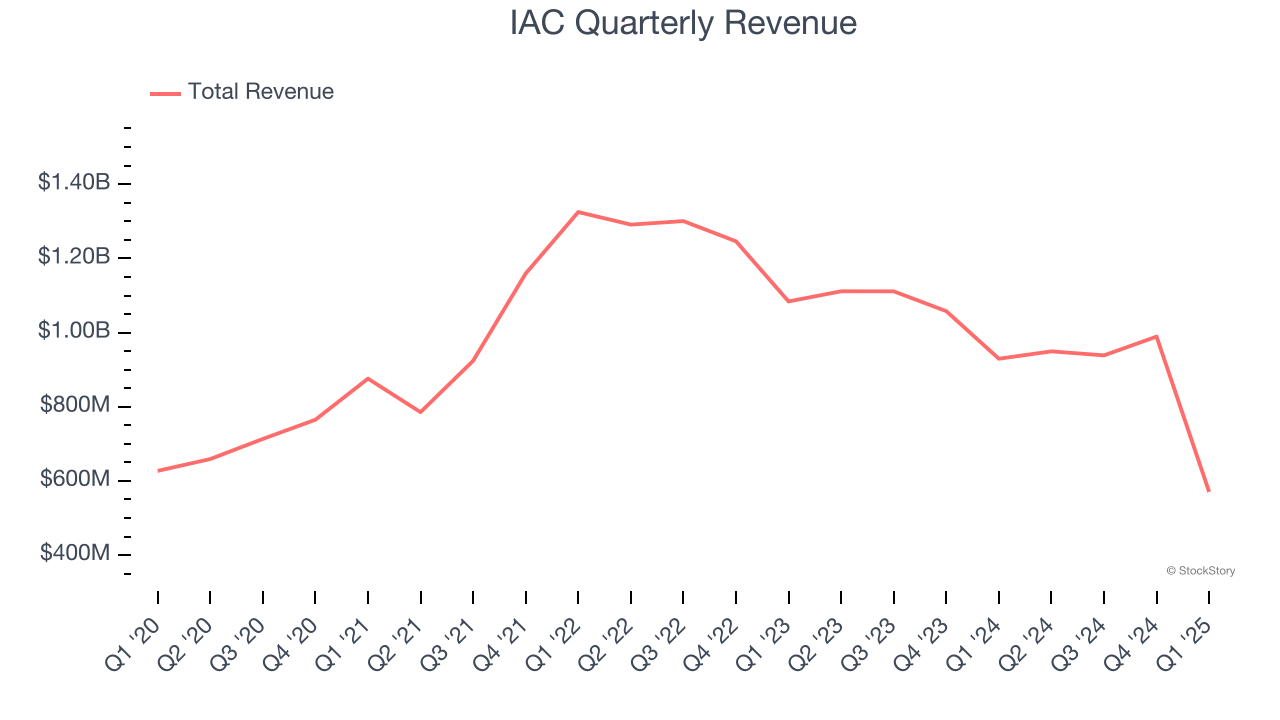

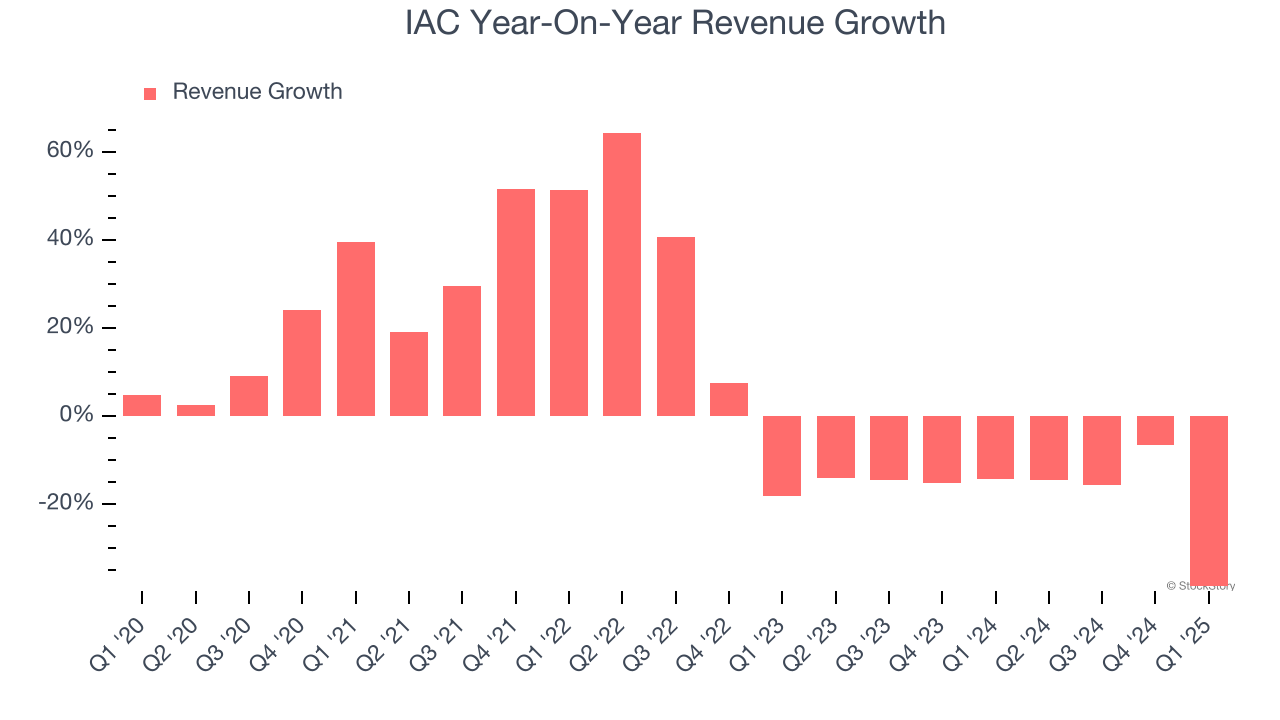

Digital media conglomerate IAC (NASDAQGS:IAC) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 38.6% year on year to $570.5 million. Its GAAP loss of $2.64 per share was 30.1% below analysts’ consensus estimates.

Is now the time to buy IAC? Find out by accessing our full research report, it’s free.

IAC (IAC) Q1 CY2025 Highlights:

- Financials this quarter are not comparable to Consensus expectations as there was a completed spin-off of IAC’s ownership stake in Angi on March 31, 2025. Angi Inc. results are reflected as discontinued operations in Q1 2025 and all historical periods

- Revenue: $570.5 million vs analyst estimates of $809.2 million (38.6% year-on-year decline, 29.5% miss)

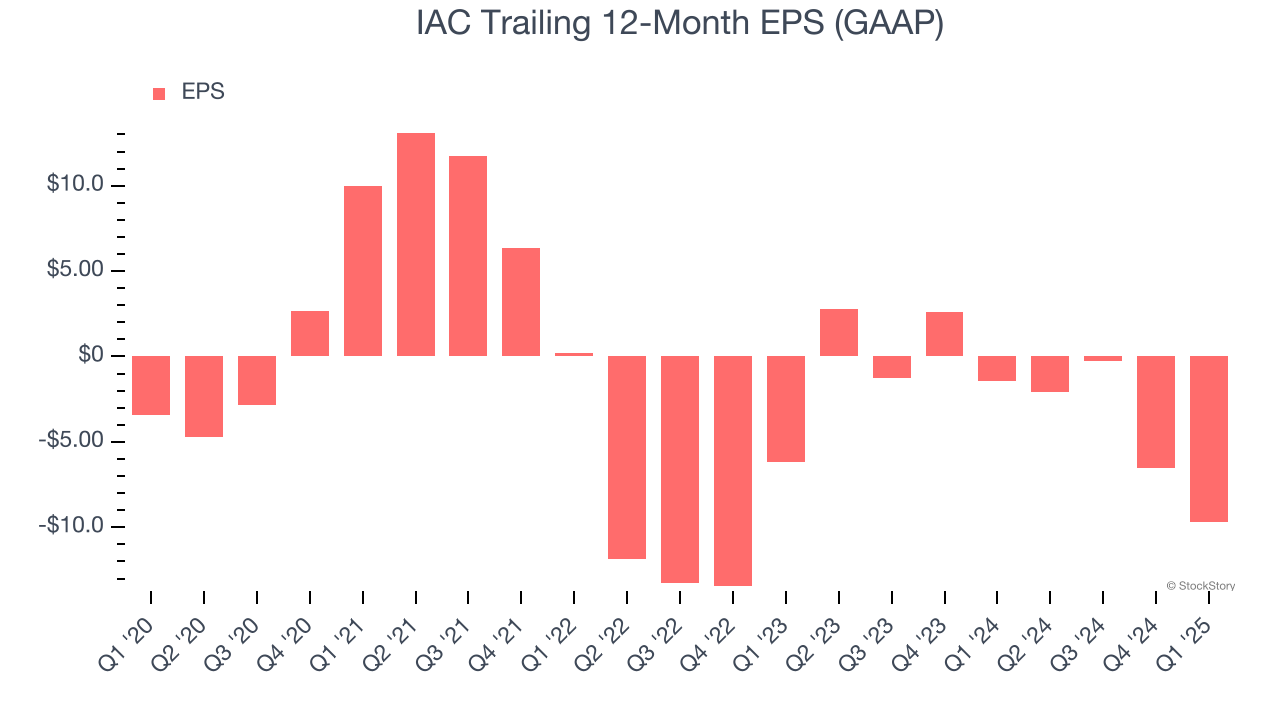

- EPS (GAAP): -$2.64 vs analyst expectations of -$2.03 (30.1% miss)

- Adjusted EBITDA: $50.9 million vs analyst estimates of $19 million (8.9% margin, significant beat)

- EBITDA guidance for the full year is $267.5 million at the midpoint, above analyst estimates of $251.1 million

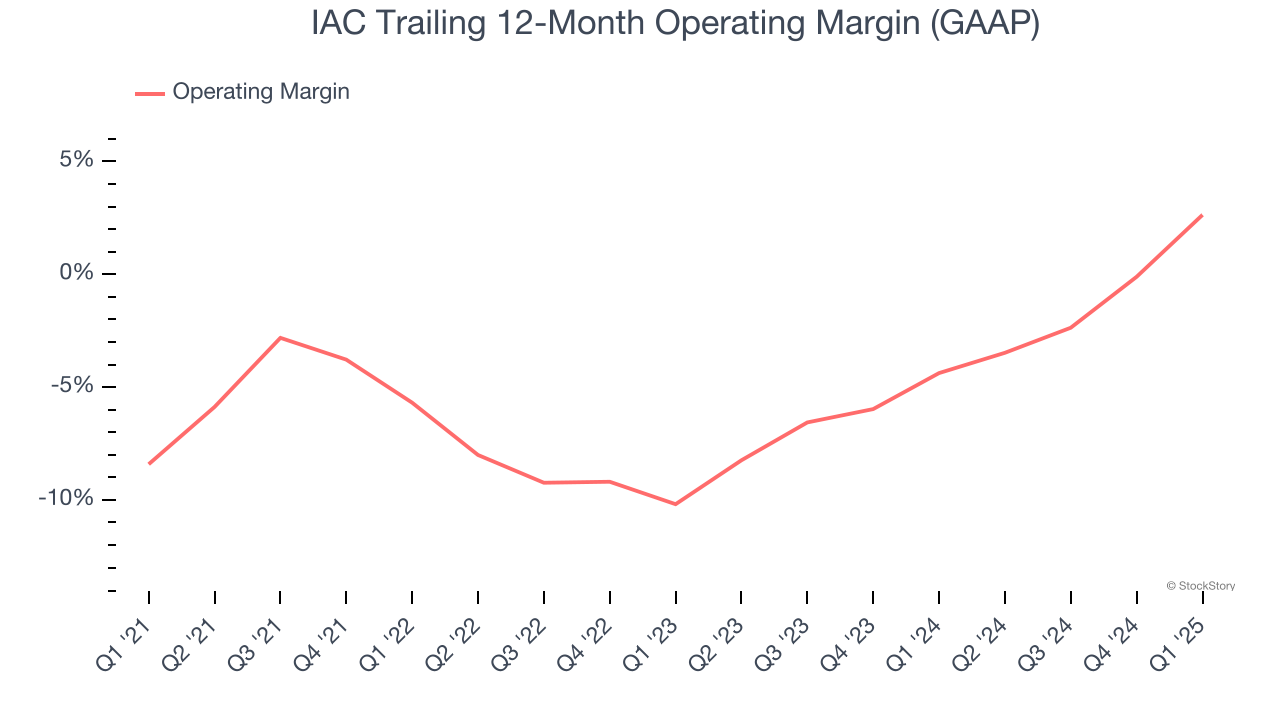

- Operating Margin: 6.3%, up from -6.4% in the same quarter last year

- Free Cash Flow was -$4.6 million, down from $48.34 million in the same quarter last year

- Market Capitalization: $2.83 billion

Company Overview

Originally known as InterActiveCorp and built through Barry Diller's strategic acquisitions since the 1990s, IAC (NASDAQ:IAC) operates a portfolio of category-leading digital businesses including Dotdash Meredith, Angi, and Care.com, focusing on digital publishing, home services, and caregiving platforms.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $3.45 billion in revenue over the past 12 months, IAC is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, IAC’s 6.3% annualized revenue growth over the last five years was decent. This shows its offerings generated slightly more demand than the average business services company, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. IAC’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 16.3% over the last two years.

This quarter, IAC missed Wall Street’s estimates and reported a rather uninspiring 38.6% year-on-year revenue decline, generating $570.5 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.6% over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Although IAC was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 5.5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, IAC’s operating margin rose by 11 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, IAC generated an operating profit margin of 6.3%, up 12.6 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

IAC’s earnings losses deepened over the last five years as its EPS dropped 23.1% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, IAC’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, IAC reported EPS at negative $2.64, down from $0.52 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast IAC’s full-year EPS of negative $9.67 will flip to positive $1.09.

Key Takeaways from IAC’s Q1 Results

Financials this quarter are not comparable to Consensus expectations as there was a completed spin-off of IAC’s ownership stake in Angi on March 31, 2025. Angi Inc. results are reflected as discontinued operations in Q1 2025 and all historical periods. The stock remained flat at $35.26 immediately after reporting.

IAC’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.